As significant emitters of carbon dioxide, refineries are rarely mentioned in a green or decarbonisation context – but upcoming regulatory changes mean their repositioning provides new opportunities for the beleaguered hydrogen sector to grow.

According to the report, “Isn’t it ironic? How Europe’s oil refiners could offer a route to scale up green hydrogen”, European refiners are set to require ~0.5 million tonnes of green hydrogen annually by 2030 to comply with EU regulations, replacing about 30% of current CO2-emitting hydrogen production.

High costs have provided a brake on green hydrogen projects, but the new EU regulations offer a solution to launching this carbon friendly technology at scale, according to the report.

Source: Horizon / Wood Mackenzie

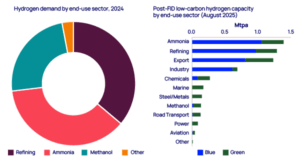

Refining represents one of the largest hydrogen opportunities globally, which, alongside ammonia and methanol production, accounts for 98% of current demand.

The latest revision of the EU’s Renewable Energy Directive (known as RED III), favours green hydrogen over blue hydrogen, helping to minimise the delays and cancellations now all too common when it comes to green hydrogen globally.

“European refiners are set to become significant producers or buyers of green hydrogen, initially to decarbonise the refining sector and its derivatives as fuel for marine and aviation,” said Alan Gelder. “Numerous green hydrogen projects have already targeted the sector.”

European refiners have been part of the EU Emissions Trading Scheme for more than a decade and are charged for the CO2 they emit beyond a certain free allowance.

This allowance will gradually be eliminated over time, raising the cost for refiners. Producing green hydrogen on site using renewable-powered electrolysis would eliminate many of those CO2 emissions and emission-related carbon costs.

The report finds that of the 6 mtpa of low-carbon hydrogen capacity that has taken a final investment decision (FID), European refineries have already committed more than $5bn of capital.

Refiners demonstrate strongest market appetite

Recent EU Hydrogen Bank (EHB) auction results reveal refineries’ commitment to green hydrogen adoption, with the sector showing the highest willingness to pay premium prices at an average levelised cost of hydrogen of $9.23/kg – demonstrating their requirement to meet regulatory mandates.

This compares favourably with Wood Mackenzie’s asset-level modeling of refinery-targeted projects, which produces costs of $7.04-$8.30/kg.

Average green hydrogen costs dropped 18% in the latest EU auctions, with German bids falling more than 55%. However, progress remains uneven across the bloc, with slow national adoption of RED III legislation hampering project development in many member states.

Uncertainties remain over the EHB auctions however. The European Commission is to reallocate funding from the first two auctions to reserve projects that initially missed out, after three winners pulled out.

Beyond Europe, Indian refineries recently announced they will invest ₹2 trillion ($23bn) in green hydrogen projects in the next few years.

Long-term growth lies in transport fuels

While refinery decarbonisation offers the strongest near-term investment case, the marine and aviation sectors present massive long-term growth opportunities for green hydrogen derivatives.

The EU’s ReFuelEU Aviation framework alone requires sustainable aviation fuel to power 6% of the jet pool by 2030, with 1.2% coming from green hydrogen-based e-fuels.

By 2050, sustainable aviation fuel mandates could require 8 million tonnes of green hydrogen – representing a compound annual growth rate of over 15% for this sector alone.

Similarly, Europe’s FuelEU Maritime Regulation and the International Maritime Organization’s Net Zero Framework are driving interest in hydrogen-derived marine fuels.

“The opportunities for low-carbon hydrogen have come full circle,” said Murray Douglas, Vice President of Hydrogen Research at Wood Mackenzie.

“The traditional sectors of refining, ammonia and methanol are showing the most progress, ahead of the many other new demand sectors being touted for hydrogen. Parts of the refining sector can be decarbonised quickly – and at an acceptable cost. But it requires policy intervention to lower green hydrogen production costs and increase the refineries’ offtake.”

Douglas added, “Marine and aviation hold much of the long-term potential for hydrogen derivatives, as these sectors are the most challenging to electrify. The challenge lies in competing fuels, the costs of production and the final shape of the policies providing support.”

Policy gaps remain key barrier

Despite the progress, significant hurdles remain. Current EU policy requires RFNBOs to account for only 1% of transport sector energy use by 2030 – a modest target that reflects the challenges in expanding supply. Member states have been slow to transpose RED III into national legislation, creating regulatory uncertainty that has slowed project development across most of the EU.

The report concludes that while European refiners could play a critical role in scaling up the green hydrogen industry, success depends on continued cost reductions and stronger policy support to fully kick-start demand across the continent.